- Trump to cut off Chinese cooking oil?…

- The strange relationship between stocks, bonds and gold…

- Gold’s smashing records right now. But DON’T buy physical gold right now. Click here to discover a much more powerful strategy to collect an extra $12,000 to $15,000… or even $52,000 a year from gold… without buying actual gold.

Dear Reader,

The president frightened the horses yesterday. How?

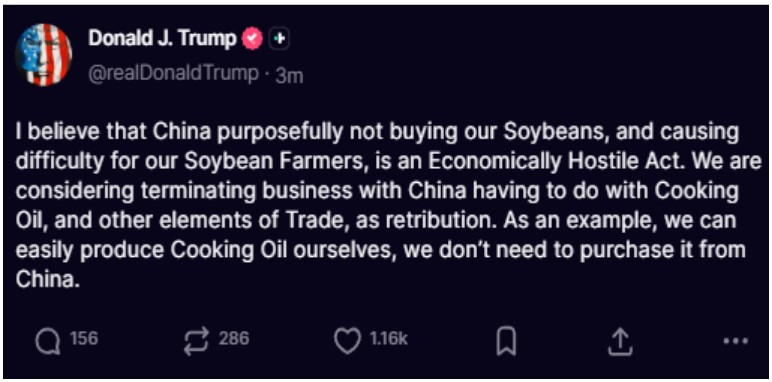

By threatening to chase Chinese Cooking Oil from these shores — in retaliation for China’s “Economically Hostile Act” against American Soybean Farmers:

The stock market hemorrhaged some $450 billion within seven minutes of the president’s dispatch.

Stocks subsequently discovered their fighting spirit… and clawed their way up the wall of worry.

The Dow Jones Industrial Average closed trading 202 points above zero.

The S&P 500 and Nasdaq Composite posted losses — yet tolerable losses.

Gold, meantime, advanced $28 yesterday, to $4,161.

At the same time, the 10-year Treasury yield retreated to 4.022%.

Year-to-date, yields have decreased some 12%.

Mixed Signals

Bond yields and bond prices exist in a state of antagonistic polarity.

If bond prices increase, bond yields decrease. If bond prices decrease, bond yields increase.

Imagine a seesaw in swinging dynamism — now you understand the bond price/bond yield relation.

Thus the declining 10-year yield corresponds to a price increase.

The rising price means investors are flocking into Treasurys. They are not fleeing Treasurys.

Since Treasurys are dollar-denominated assets, we can only conclude that investors are not fleeing the dollar as such

Yet gold trades at record levels.

Is not a record gold price a repudiation of the dollar?

In general — in general — I incline towards the theory that it is a repudiation of the dollar.

In yesterday’s article I advanced that theory.

Interesting…

Yet here the crackerjacks of Fisher Investments point to a skunk in my theoretical woodpile:

- Supposedly, gold reaching new highs signals investors and central banks’ preferring the shiny metal over the US dollar and Treasurys as a safe haven…

- Yet … there just isn’t strong evidence people are abandoning the dollar and dollar-based assets the way many claim. Historically speaking, the dollar isn’t that weak. Nor are US Treasury yields sky high, which many associate with rising risk…

- Treasury yields… are down year to date and well below levels seen in the 1970s and 1980s. This doesn’t scream “major exodus” to us.

I must concede the point. The facts do not scream “major exodus.”

The gold price nonetheless wings along at record heights.

I do not believe that political risk, geopolitical risk, trade risk, or other traditional lifters of the gold price account for it.

A Head-Scratcher

All the while, both gold and the stock market are soaring in tandem… as if on eagles’ wings.

What should we deduce from it?

Puzzlement, perhaps. Here is Barron’s:

- The tight correlation between the gold market and stock market leadership is unusual. Bank of America points out that in the third quarter, small-caps and the tech and communications services sectors were the best stock market performers. Those sectors outperformed along with gold, the best performing asset class, up 16.4% in that quarter.

- Those particular sectors have not really had much correlation with gold at all, going back to 1989, BofA said.

Here Mr. Christopher Louney, commodities strategist at RBC Capital Markets, hazards an explanation:

- Investors, on the one hand, are afraid of missing out and they are investing in the risk-on [stock] market. And at the same time they recognize the uncertainty and they are making investments in gold.

Perhaps there is justice here. What we are witnessing may simply be a hedging of wagers.

Is It Just the “Everything Bubble?”

Now let us mix bonds into the figure.

Recall, bond prices are also rising. Thus we find stocks, bonds and gold going on on positive trajectories.

What does this curious condition bode for the stock market? CNBC:

- Put simply, [investors] believe when safe-haven gold and bonds are going higher, things are not right with the world, and stocks should go lower.

- But history shows this phenomenon of the three trading in unison ends up being bullish for stocks, proving equity investors correct who bought while the two other assets were supposedly flagging trouble ahead.

Just so. Yet history is not an infallible instructor.

The Short Run… and the Long Run

Regarding the gold price:

Goldman Sachs estimates that gold could leap to $5,000 should merely 1% of the privately owned Treasury market flee into gold.

Will gold outshine stocks and bonds in the days to come?

In the short term, I do not know.

In the long term — however — I believe I do know.

One of these assets has withstood thousands of years of earthly history.

It is not stocks. Nor is it United States Treasury bonds.

Only one choice remains.

Regards,

Brian Maher

for Freedom Financial News